Credit Cards: How they work and how to use them

Credit card companies are not your friend — sad, but true. They are in the business of providing super-tempting perks to people and lending them money KNOWING that some will misuse their credit cards, resulting in lots of interest for the card user and a profit for the card company.

Credit card company: 1; You: 0. Let’s change that.

What are credit cards?

Credit cards are standing lines of credit that you can pull from. Using a credit card over your debit card can be beneficial — mainly through earning reward perks and protecting your purchases against fraud. For these reasons, credit cards can be great — when used properly. Unfortunately, it’s extremely easy to overspend on a credit card. So, be sure to monitor your spending!

Don’t overspend. Don’t be that person. Let me explain.

That really high number on your credit card portal — that’s your “available credit”. That number is the maximum amount the credit card company has determined that they are comfortable lending to you at any given time. That number is NOT the recommended amount you can (or should ) spend at any given time — not even close.

Let’s take a look at this example. This month your “available credit” is $10,000 and you received $2,000 last Friday in your paycheck. Your $2,000 paycheck is all you can spend until your next paycheck. Even though your available credit line says you can spend the full $10,000. That $2,000 is IT. Spend any more, and you’ll put yourself in a debt sinkhole.

On top of that, you probably shouldn’t even spend the full $2,000 because you need to save some for your future. We say all of that to say, spend less than you earn (more on that in another blog — stay tuned!). That’s the number one lesson in personal finance.

But my minimum payment is way lower than that!

Don’t let your “minimum payment” amount fool you. This number is another tool credit card companies use to confuse you into paying less than you should. It’s called a “minimum payment” for a reason. The “minimum payment” is the smallest payment you could make that month and not be reported as late to the credit bureaus. This is NOT the number that will prevent you from paying interest. In fact, any money you still owe to the credit card company over and above what you pay to them (like the minimum payment) is money you will pay interest on during the following month.

In the previous example, you might think you can get away with spending $3,000 instead because you have more than enough available credit and your minimum payment is only $200. DON’T DO IT! That’s exactly where they get you. They make the minimum payment number very appealing and it makes you want to pay just that amount right away. But that’s like Odysseus and the Sirens — very dangerous. As soon as you pay anything less than your full statement balance, BAM — you’re now paying that skyhigh interest rate! So it’s good to keep in mind :)

You might not even know you’re overspending

You might overspend using credit cards and not realize it. Just because you’re paying more than the minimum payment each month or not being charged interest on your credit card doesn’t mean you’re building bad credit card and spending habits.

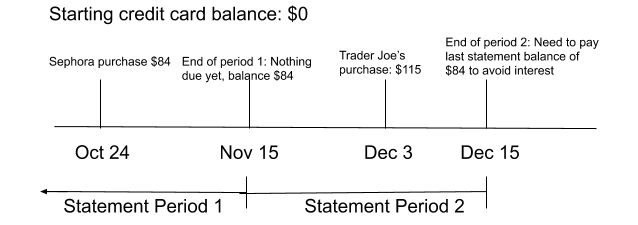

Check out the chart below to better explain how overspending works. Imagine you make a Sephora purchase on October 24th for $84 and put it on your credit card. To avoid interest, you won’t need to pay back the credit card company for the $84 purchase until December 15th. But now you’re playing a shell game. By not paying that $84 off until December 15th, you’ve managed to spend $84 of your December paycheck already all the way back in October.

As you might imagine, this is bad. You are literally spending money you don’t have (aka “Future You Income”) months before you actually earn it. Compounding that, when December comes around you need to of course pay for your expenses in December, but also for those expenses way back from October. If you kept operating in this manner, you would always be going to work today to pay for your past — not building your future.

Using credit cards this way makes it very difficult (if not downright impossible) to get ahead financially and very easy to go into credit card debt without realizing it. Spending this way is straight up the wrong way to use them. One missed payment and you’re already on the path to digging a deeper sinkhole of debt. This doesn’t even include the interest that the credit card companies will charge you. This debt cycle makes your future dreams of going back to school, paying for a wedding or putting a downpayment on a home disappear farther and farther out of reach.

So what should I do instead?

Play the credit card game your way. Pay your credit card at a frequency that makes sense for you — every evening, every week or every two weeks. You don’t have to wait for the credit card company’s due date to get the points and perks. Pay back your credit card company right away and in full with real money from your checking account.

By making frequent credit card payments, this will let you know if you have enough money in your checking account at any time to pay purchases you make on your credit card — making it then not possible to spend more than you’ve earned. Phew!

You can find one that’s right for you here. Credit card company: 0; You: 1.

Need help finding a credit card spending plan that makes sense for you? Schedule a free 15-minute intro call for one-on-one guidance to ensure you’re on the right financial track to build financial momentum and work to achieve your life goals!

Sign up for blog updates to stay on top of the latest Momentum blog posts!